Institutional Adoption Accelerates

March highlighted a powerful shift toward institutional adoption, with major players doubling down on tokenization and blockchain infrastructure.

The New York Stock Exchange partnered with Securitize to build a 24/7 tokenized securities trading platform, enabling stocks and ETFs to be issued directly onchain. Meanwhile, Franklin Templeton and Ondo Finance are launching tokenized ETFs accessible via crypto wallets—no brokerage needed.

In another breakthrough, Coinbase partnered with Better to introduce crypto-backed mortgages supported by Fannie Mae. This is a major step toward bridging crypto and real-world assets.

Additionally, Nasdaq and Talos are working on tokenized collateral systems, further connecting traditional finance (TradFi) with crypto markets.

Markets Shaken by Geopolitics

This month, global markets were heavily influenced by geopolitical tensions—especially involving Iran and the United States under Donald Trump.

Conflicting statements about military action and negotiations caused extreme volatility across:

- Crypto markets

- Equities

- Commodities (especially oil)

Oil surged nearly 15% during the month, while Bitcoin hovered around $68,000, struggling to gain momentum. The Strait of Hormuz situation remains a critical factor, with markets reacting almost instantly to political updates.

Investor sentiment remains in extreme fear territory, highlighting just how dominant macro events have become in shaping crypto trends.

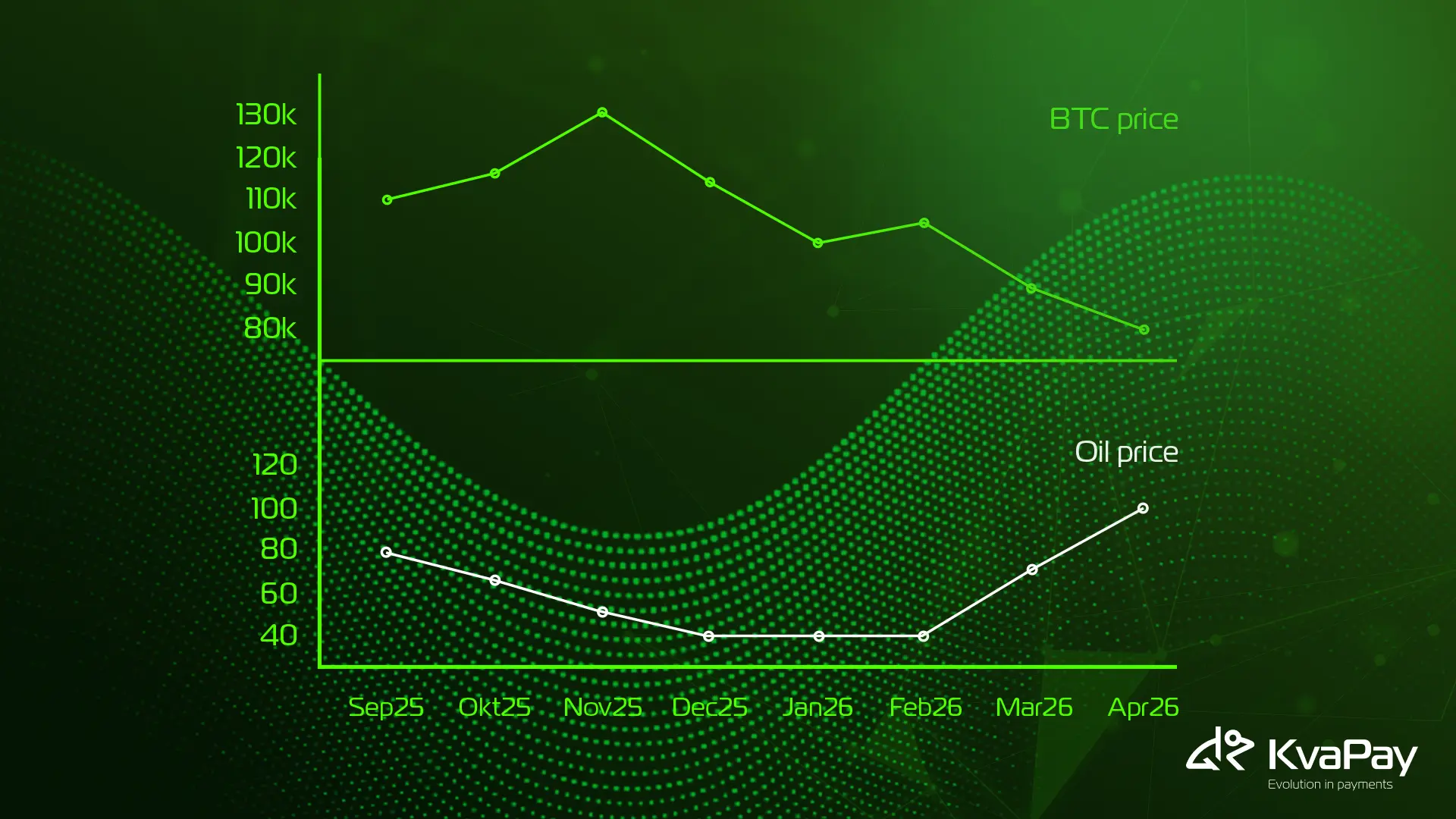

Bitcoin vs Oil: A Key Narrative

One of the most important insights this month is Bitcoin’s performance relative to oil.

Bitcoin is down 65% against crude oil since September, significantly underperforming compared to its USD decline. With oil surpassing $105 per barrel, historical patterns suggest potential downside risks for Bitcoin—but the correlation remains uncertain.

This reinforces a key takeaway: Crypto is no longer isolated. It is deeply tied to macroeconomic and geopolitical forces.

Onchain Growth & Emerging Revenue Models

Onchain activity continues to evolve rapidly, with new revenue models emerging across protocols.

Polymarket is expanding its fee structure, potentially pushing monthly revenues toward $30M–$50M, placing it among top crypto revenue generators.

At the same time, Hyperliquid is seeing record activity. Its HIP-3 markets reached $5.4B in trading volume, driven largely by commodities like oil and gold amid geopolitical uncertainty.

This trend signals a shift toward real-world asset trading onchain, especially during high-volatility periods.

Fund Flows & Market Pressure

Digital asset investment products recorded $230M in inflows, with Bitcoin dominating. However, Ethereum saw notable outflows, breaking its previous positive streak.

Major players are taking different approaches:

- Strategy continues aggressively accumulating Bitcoin and raising capital (up to $44B potential)

- MARA Holdings sold over 15,000 BTC to reduce debt

This divergence highlights growing pressure on miners while institutional buyers continue long-term accumulation strategies.

Europe Moves Toward Tokenized Finance

The European Central Bank introduced the Appia roadmap, aiming to build a tokenized financial system in Europe.

At its core is Pontes, a DLT-based settlement solution expected in Q3 2026, designed to connect blockchain infrastructure with Europe’s payment systems.

This initiative aligns with the upcoming digital euro, signaling Europe’s serious commitment to blockchain-powered finance.

Euro Stablecoins on the Rise

Euro-denominated stablecoins are gaining traction, now making up:

- Over 80% of non-USD stablecoin supply

- Around 85% of transaction volume

EURC is leading the market, supported by integrations with major payment networks. This growth is largely driven by Markets in Crypto-Assets Regulation, which brought regulatory clarity and enabled adoption across Europe.

Final Thoughts

March 2026 made one thing clear:

Crypto markets are no longer driven solely by innovation. They are increasingly shaped by institutions, regulation, and geopolitics.

From tokenized ETFs and crypto-backed mortgages to war-driven volatility and Europe’s digital finance push, the industry is entering a new phase where macro and blockchain are deeply intertwined.

As we move forward, all eyes remain on geopolitical developments, because right now, they are the single most important force in the market.

Buy your favourite cryptocurrency with KvaPay. Start investing in your future today.